The fourth and most recent Tax Expenditure Report published by the Treasury in August 2023 establishes that preferential rates and corporate exemptions constitute $22 billion of the $24 billion of tax expenses reported in Puerto Rico. The trend shown by the Report is that in Puerto Rico fiscal expenditures continue to increase.

Given this panorama, and considering the great weight that preferential treatment and tax exemptions to foreign corporations have as an incentive to do business in Puerto Rico, Open Spaces (EA) warns about the effect that the Global Minimum Tax could have on the economy of Puerto Rico (GMT, Global Minimum Tax) that is discussed around the world.

On the other hand, the analysis of Espacios Abiertos presents for the first time a look at fiscal expenditures at the municipal level.

Access the most recent analysis and report here (Spanish version) prepared by Wilmarí de Jesús, public policy analyst at Espacios Abiertos. For him summary of findings click this link. For the English version of the Report, access this link.

____

For your analysis, EA It is based on the report published by the Treasury, titled in English Puerto Rico Tax Expenditures 2024 (PRTER) and the standards for audited statements established by the Governmental Accounting Standards Board (GASB) -independent organization that sets accounting and financial reporting standards for state and local governments in the United States. Furthermore, with regard to the fiscal expenses of the municipalities, since these are not part of the PRTER, EA takes information from the audited financial statements of all municipalities that seek to comply with GASB 77, a standard that came into effect on December 31, 2015.

Even with the progress that the publication of the PRTER has represented since 2019 and the compliance of the majority of municipalities with GASB 77, there is still a need for greater transparency, detail and granularity in the information on the fiscal impact of contributory benefits. Particularly, to achieve a thorough evaluation and the corresponding cost-benefit analysis of each of the credits, exemptions and incentives granted. Accurate information is essential so that legislators, government officials and citizens can evaluate and make informed and timely decisions regarding fiscal policy and the effective administration of Puerto Rico's budget and resources.

Furthermore, since 2022 EA has insisted on the need to present the PRTERs in an open data format that allows the analysis of these measures with complete, reliable and easy-to-process data. Despite the challenge that the publication format has represented, EA has been given the task of emptying the information on the more than 400 types of expenses included in the PRTER, into interactive data panels that make it easier for anyone to search. Interactive dashboards can be accessed here.

What are fiscal or tax expenses?

The federal budget law of 1974 (Congressional Budget Act of 1974) defines tax expenses (tax expenditures) as the loss of income that the government has as a result of laws that reduce or even eliminate the normal tax liability of a group of taxpayers or some defined economic activity.

This preferential treatment can take several forms; such as exclusions, exemptions or special deductions that reduce the income subject to tax, or they may be credits, decrees, deferrals and special tax rates provided.

By causing reduction in government revenue They are designated as “expenses” under the premise that a dollar that stops entering the treasury is economically equivalent to a dollar of public spending, which is why the term “tax expenses” is used..

_______

finds themzgos from EA on PRTER 2024 and fiscal expenditures of the central government:

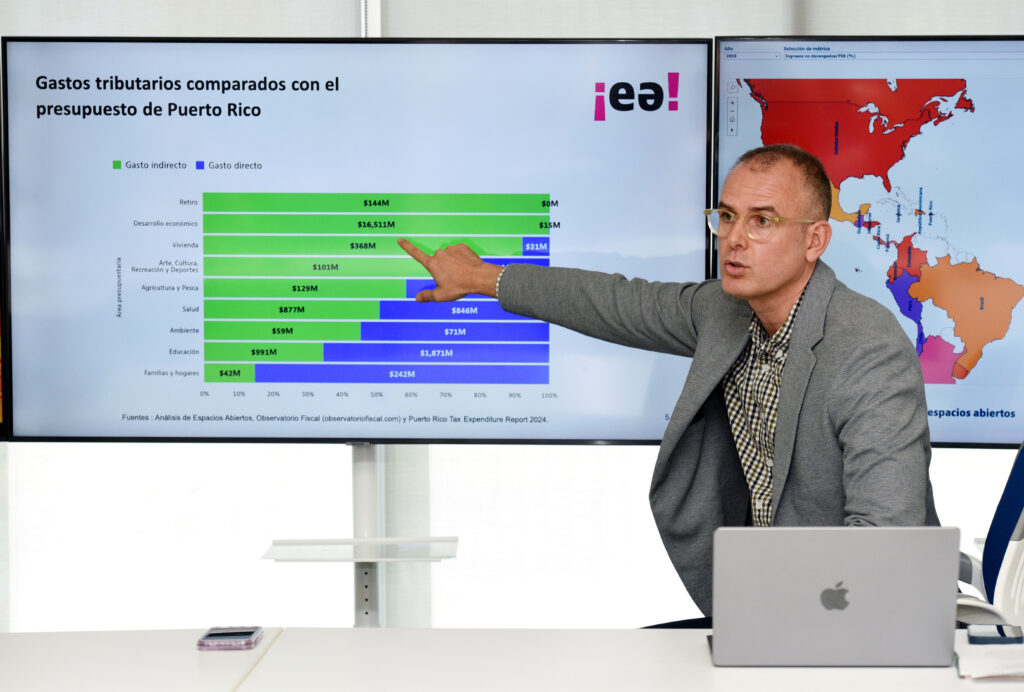

72.52% ($22,222.80 million) of unearned income from tax expenses in 2021 correspond to contributions from corporations.

In 2021, a total fiscal expenditure of $24,538.60 million was estimated, with 67.28% ($16,510.50 million) allocated to the area of economic development.

In 2021, the government opted for indirect or tax expenses over direct expenses in areas such as economic development, retirement and housing.

In the PRTER 2024, 61.46% of tax expenditures are estimated, showing an improvement compared to the 53.7% presented in the PRTER 2023. However, Puerto Rico is still below the world median in terms of the proportion of tax expenditures for which estimates are provided.

EA's key findings on municipal tax expenditures:

- The lack of centralized visibility on tax expenditures at the municipal level compared to reports at the state level is highlighted. Currently, 54 of the 78 municipalities (69.23%) contain complete or partial estimates of tax expenditures.

- Municipalities stop accruing at least $539,163,263 million in additional tax expenses to the 24,538 million identified in the PRTER 2024.

- Of the $539.1 million of unearned revenue, at least $226.3 million (41.98%) corresponds to personal property taxes, followed by $172.4 million (31.9%) to real property taxes.

- State laws play a dominant role by enabling 86.84% of total tax expenditures, equivalent to $468,228,427 million.

- The municipality of Carolina leads with $146,266,526 in unearned income, followed by Guayama with $59,580,476 and Vega Baja with $36,601,553.

- In six cases (Guayama, Juana Díaz, Vega Baja, Carolina, Gurabo and Cidra) tax expenses exceed their municipal budget. In 11 cases, tax expenditures exceed 50% of the municipal budget.

EA Recommendations

Pass a law to ensure detailed annual reporting on tax expenditures, at both the state and municipal levels, that comply with standards and best practices, including specific information on tax exemptions granted, the laws that support them, and unearned income figures. (At the level of the Legislative Assembly, bills for these purposes have been presented and approved, however these have been vetoed by the Executive).

Include detailed reports on tax expenditures in the government budget approval process so that legislators and government officials have solid information in a timely manner to make decisions about the allocation of resources and the continuation of tax exemptions. In this way, transparency and effective fiscal management are promoted.

-

- In 2023, the tax expenditure report was published on June 30, 2023, one day after the approval of the 2023-2024 budget by the Legislative Assembly, and six months after the deadline established by the Fiscal Control Board for the Fiscal Plan Government Certificate.

Use updated data in estimating tax expenditures for greater precision and real effectiveness of the projections.

The incorporation of municipal tax expenditures in all municipal audited states, in accordance with the provisions of the GASB 77.

___________

Espacios Abiertos began in 2017 to insist on the need to know, disclose and analyze tax expenditures in Puerto Rico. Between 2018 and 2019 she took a case to the Supreme Court seeking disclosure of these expenses. In September 2019, for the first time, the government of Puerto Rico published a tax expenditure report, something that the federal government, the states and many countries had done since the 70s. To date, four expenditure reports have been published in Puerto Rico. prosecutors, qualified in English Puerto Rico Tax Expenditures Reports (PRTER).

By ensuring that all the necessary data is available in the appropriate forms with detailed information on tax expenditures, it will result in better evaluations of the effectiveness of fiscal policies and that the necessary adjustments can be made in a timely manner.

# # #